Are we at an inflection point for technology growth?

- 05 July 2021 (5 min read)

Technology has attracted a lot of attention this year, with higher interest drawing some concern over valuations. While semiconductor shortages have highlighted the world’s dependence on technology, investors have also been looking to companies which are poised to benefit from the reopening of the global economy.

Thus far, corporate earnings and guidance for 2021 have been encouraging from the companies we invest in. Within our strategy, the biggest positive surprises have come from a wide variety of sectors, supporting our view that we are at an inflection point in terms of the growth acceleration we see in various advanced technologies. Areas like 5G, artificial intelligence and digital banking offer new opportunities for companies within the technology sector and new opportunities for investors.

More broadly, the macroeconomic picture is improving. The US economy continues to perform strongly; first quarter (Q1) GDP came in at its fastest rate since 2003, while S&P 500 first quarter earnings-per-share growth is on track to exceed 45%, more than twice the growth expectations before Q1 earnings season begun.1

New long-term drivers of growth

We already see 5G making a difference to company results, with Apple launching several new products, including its first 5G handset. The development of 5G has implications right across a range of sectors, from tower operators to specialist chip manufacturers such as Qualcomm, which now receives royalties for its intellectual property from every major handset manufacturer in the world.

Read more: Opportunities being created by the 5G evolution

The semiconductor industry remains critical to the global economy, with this only highlighted by the recent chip shortage. While we think current conditions could help manufacturers by supporting their pricing power, the longer-term opportunity lies in the growth of the market.

According to Gartner, worldwide semiconductor revenue rose to $466.2bn in 2020, a 10.4% increase on the year before. Growth has remained strong this year, with the Semiconductor Industry Association reporting that chip sales rose by 17.8% in the first quarter of this year compared to the same period a year ago. Several trends reinforced by the pandemic – i.e. the rise of cloud computing, the internet of things and industry digitalisation – have boosted end demand for chips. Investors continue to underappreciate other growth drivers in our view, such as the importance of chips in electric vehicles, which are critical in everything from batteries to braking systems.

COVID-19 consequences to continue

While the pandemic clearly boosted the technology sector, there is still plenty of room for further growth. As the CEO of PayPal commented, most estimates of e-commerce have been pulled forward three to five years as a result of the pandemic. PayPal is now seeking to capitalise on the increased engagement it has seen over the past year and is putting in place plans to accelerate the launch of new financial products and services, such as its ‘pay later’ scheme.

- IFNvdXJjZTogQmxvb21iZXJnLCBGYWN0U2V0LCBBWEEgSU0sIEp1bmUgMjAyMS4=

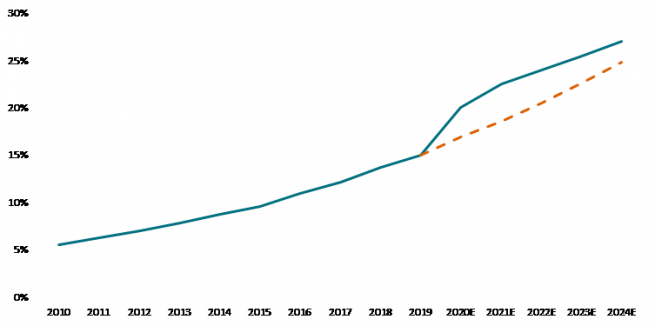

Card-based or mobile-wallet based transactions are rapidly becoming the first choice for the majority of consumers, regardless of transaction size. In a report last year, Gartner even went so far as to say that global cash in circulation would reduce in 2024 for the first time in decades.1 The move away from cash is a long-term secular trend which is far from over, rather than a one-off boost which compresses future growth into a shorter time-span.

Quality companies justify a premium

Technology has undeniably had a good run – both over the past year and even before the pandemic. While the urge to take profits is understandable, technology remains a very attractive part of the market, able to grow over and above the long-term rate of the economy. We continue to believe that good quality growth companies justify a premium and that our holdings will be able to grow into their valuations over time.

At the time of writing, for those companies in the MSCI World Index (representing the broader market) that have reported their first-quarter numbers, 69% have reported better-than-expected revenues and 75% reported better-than-expected earnings. For the technology component of the same index, the results were 79% and 83%, respectively.2

The price action we have seen over the first half of 2021 will of course happen from time to time, and we will sometime trim positions when they look to have gotten ahead of themselves, as we did with Zoom late last year. This does not change our view on technology’s secular growth opportunity, however, and that the fundamentals of the businesses we invest in remain very solid.

- U291cmNlOiBCbG9vbWJlcmcsIEZhY3RTZXQsIEFYQSBJTSwgSnVuZSAyMDIxLg==

- U291cmNlOiBHYXJ0bmVyIFJlcHJpbnQsIE9jdG9iZXIgMjAyMC4gWzJdIFNvdXJjZTogQVhBIElNLCBCbG9vbWJlcmcsIE1heSAyMDIxLg==

Disclaimer

This website is published by AXA Investment Managers Asia Limited (“AXA IM HK”), an entity licensed by the Securities and Futures Commission of Hong Kong (“SFC”), for general circulation and informational purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy, sell or enter into any transactions in respect of any investments, products or services, and should not be considered as solicitation or investment, legal, tax or any other advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities under any applicable law or regulation. It has been prepared without taking into account the specific personal circumstances, investment objectives, financial situation, investment knowledge or particular needs of any particular person and may be subject to change at any time without notice. Offering may be made only on the basis of the information disclosed in the relevant offering documents. Please consult independent financial or other professional advisers if you are unsure about any information contained herein.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee such opinions, estimates and forecasts made will come to pass. Actual results of operations and achievements may differ materially. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Information herein may be obtained from sources believed to be reliable. AXA IM HK has reasonable belief that such information is accurate, complete and up-to-date. To the maximum extent permitted by law, AXA IM HK, its affiliates, directors, officers or employees take no responsibility for the data provided by third party, including the accuracy of such data. This material does not contain sufficient information to support an investment decision. References to companies (if any) are for illustrative purposes only and should not be viewed as investment recommendations or solicitations.

All investment involves risk, including the loss of capital. The value of investments and the income from them can fluctuate and that past performance is no guarantee of future returns, investors may not get back the amount originally invested. Investors should not make any investment decision based on this material alone.

Some of the services listed on this Website may not be available for offer to retail investors.

This Website has not been reviewed by the SFC. © 2023 AXA Investment Managers. All rights reserved.